India’s small and medium businesses in Tier-2 cities can now use AI and tokenisation for finance to cut fraud, speed payments, and access credit. This article explains a practical step-by-step approach to adopt these technologies without large IT budgets.

Why AI and tokenisation matter for Tier-2 firms

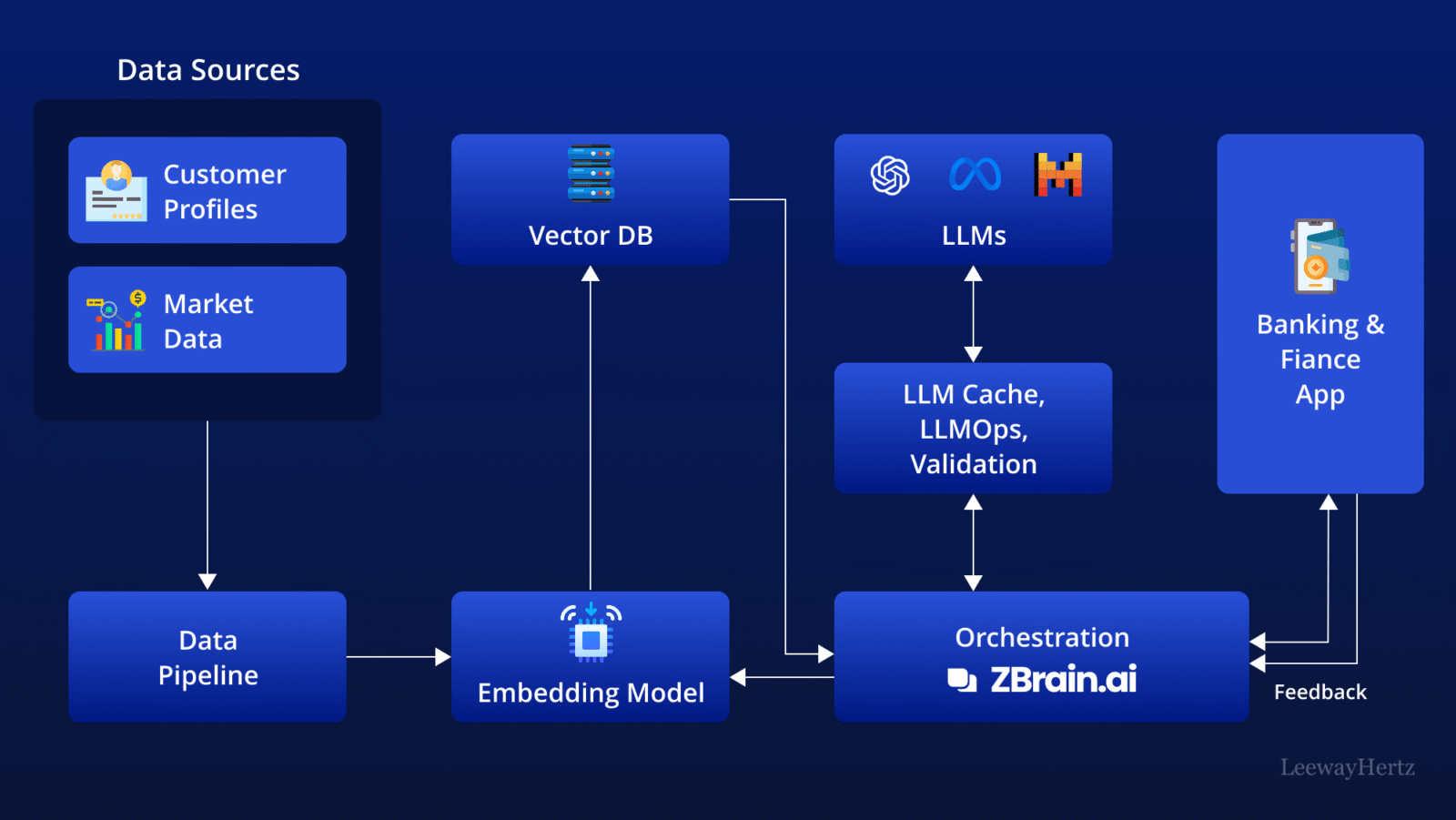

AI and tokenisation for finance together reduce payment risk and automate tasks such as credit scoring, reconciliation, and fraud detection. Tokenisation replaces raw card or account data with meaningless tokens, lowering breach risk and compliance burden. RBI guidance allows device and merchant tokenisation and requires secure authentication for sensitive flows, which makes the approach safe for local merchants. Reserve Bank of India+1

Step 1 — map a clear business use case and quick wins (secondary keyword: tokenisation use cases)

Start with one measurable problem: reduce failed payments, speed customer checkout, or improve receivables. For example, a neighborhood apparel seller can deploy card or device tokenisation to enable one-click payments and reduce abandoned carts. A small distributor can use AI to classify invoices and auto-match receipts, cutting reconciliation time by days. Keep initial scope limited to one process so you can measure time and cost savings within 60 to 90 days.

Step 2 — choose the right entry tech: plug-and-play over custom builds (secondary keyword: AI for small businesses)

Use managed services from trusted vendors or your bank’s fintech partners rather than building from scratch. Many Indian acquirers and gateways now offer tokenisation as a service and integrate with popular POS apps. For AI, pick prebuilt modules for credit scoring, invoice OCR, or anomaly detection that expose simple APIs. This reduces implementation time and keeps costs predictable while meeting upcoming regulatory expectations. Jupiter Finance News+1

Step 3 — align with regulation and authentication requirements (secondary keyword: RBI tokenisation rules)

Tokenisation and AI in finance sit inside a regulated space. RBI has set standards on who can tokenise and how tokens are issued and stored, and recent digital payments guidelines are tightening authentication requirements. Ensure your provider follows RBI rules, supports additional factor authentication where required, and can produce audit trails for transactions and model decisions. If you handle cross-border receipts, verify partner banks and settlement rails are compliant with local foreign exchange norms. HDFC Bank+1

Step 4 — implement a low-risk pilot with measurable KPIs (secondary keyword: tokenisation pilot)

Run a 6 to 12 week pilot: turn on tokenisation for repeat customers or for a single product category, and enable one AI feature such as invoice OCR or a simple credit score model. Track KPIs like transaction success rate, checkout time, dispute rate, and days sales outstanding. Use A B testing where possible: keep the old flow active for a control group so you can quantify uplift and spot regressions early.

Step 5 — scale, train staff, and lock in governance (secondary keyword: AI governance small businesses)

Once the pilot shows improvement, scale by adding new product lines and more stores. Train staff on what tokens are and why they cannot access raw card data. Put simple governance in place: document who can approve model changes, schedule quarterly model performance reviews, and set thresholds that trigger manual checks. Regulatory panels have recommended leniency for first-time AI errors but emphasize strong monitoring and rollback plans, so logging and human oversight are essential. The Economic Times

Step 6 — use tokenisation and AI to unlock finance and pricing advantages

Tokenised payment history and AI-driven cashflow forecasts can help negotiate better supplier credit or working capital from local banks and NBFCs. Some lenders now accept payment tokens and verified transaction histories as evidence of recurring cashflows when underwriting small loans. Combining tokenised receipts with a short AI credit profile can shorten loan turnaround times and reduce interest premia for reliable merchants.

Practical tech and vendor checklist for Tier-2 teams

Choose providers that support device tokenisation, integrate with your POS or website, provide clear SLAs, and offer sandbox environments. For AI modules, prioritize explainability and low data requirements. Ensure vendors can export logs for audits and provide role based access controls so store managers do not need to see sensitive data.

Takeaways

• Start small: pilot tokenisation or one AI feature, measure gains, then scale.

• Use managed services and bank partnerships to minimize engineering cost.

• Comply with RBI tokenisation and authentication rules and maintain audit logs.

• Leverage tokenised payment trails plus AI forecasts to access better working capital.

FAQs

Q1. Is tokenisation expensive for small merchants?

No. Many acquirers bundle tokenisation into existing merchant services or charge a small setup fee. The business case is faster checkouts and fewer chargebacks, which typically offset costs quickly.

Q2. Will AI replace finance staff in Tier-2 businesses?

AI automates repetitive tasks and highlights risks, but human oversight remains crucial for decisions, exceptions, and customer trust. Plan for role shifts, not replacements.

Q3. How long does a tokenisation pilot take to show value?

A focused pilot can show measurable improvements in 6 to 12 weeks if KPIs like transaction success rate and DSO are tracked and compared to a control group.

Q4. Can tokenised data be used to get loans?

Yes. Tokenised transaction records and AI-generated cashflow forecasts are increasingly accepted by lenders as supporting evidence for short-term working capital.